PKP’s third straight month of positive EBITDA - Q4 production also up to 1.6M units

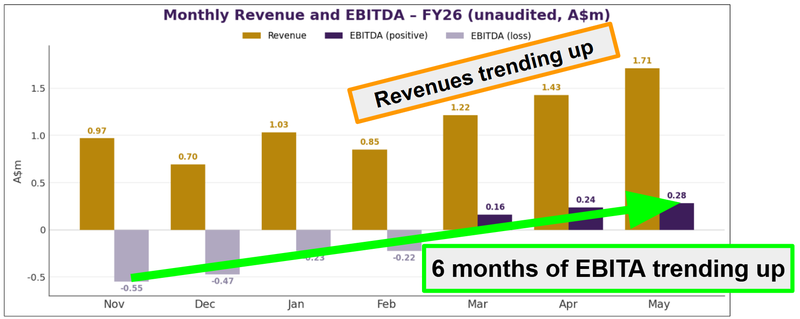

Our "picks and shovels in a gold rush" Investment for the THC drinks sector, Peak Processing (ASX: PKP), just reported its third consecutive month of positive EBITDA.

PKP has now hit positive EBITDA in March, April and May.

A total of ~$676K in EBITDA across the three months with revenues also on the up to ~$1.71M in the month of may.

(source)

On production, PKP now expects Q4 FY26 to reach ~1.6M beverage units on confirmed customer purchase orders.

That's up from the ~1.4M originally guided in March, and a further step up on the ~1.5M flagged at the May raise - so the Q4 forecast has now been lifted twice in a single quarter.

We also noticed PKP confirm in today’s announcement that 30+ new product listings scheduled to launch between June and September 2026, which should keep feeding the volume line.

(source)

A nice turnaround from November last year when the company was sitting at ~$550k in negative EBITDA and revenues almost half of what was produced in May.

A quick reminder of what PKP actually does.

PKP makes THC (tetrahydrocannabinol - the active compound in cannabis) beverages on a contract-manufacturing basis.

It supplies the tasteless THC infusion and the manufacturing line, while the partner brands handle the marketing and distribution.

That’s why we call it our "picks and shovels" Investment for the sector.

PKP sells the tools to everyone in the THC drinks rush rather than aligning to a single brand.

It's the #1 THC drink manufacturer in Canada (~33% of all cans produced).

The Canadian plant in Ontario has 12M units of annual capacity and still has plenty of capacity to bring in new brand partners.

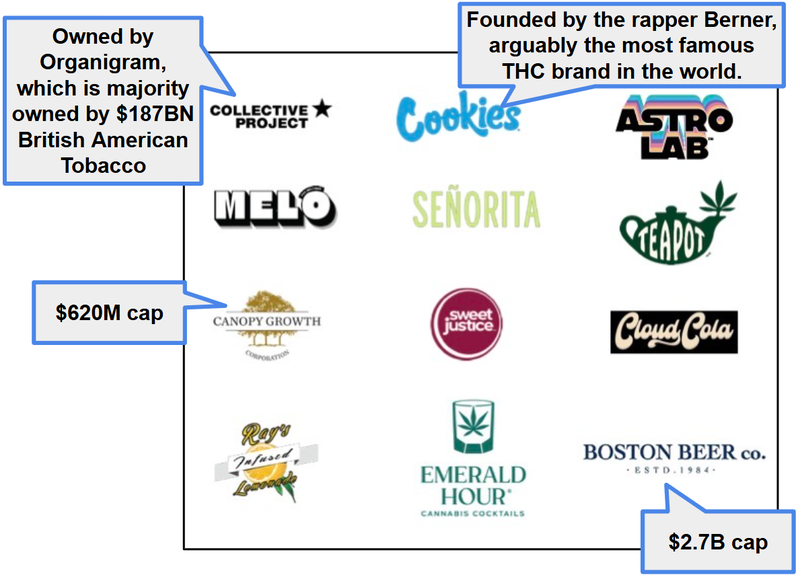

At the moment PKP manufactures drinks for companies like:

- Boston Beer Company (the non-alcoholic Twisted Tea, "Teapot") and, since December, for

- Organigram - the Canadian cannabis producer ~45% owned by ~$200BN British American Tobacco - alongside St. Peter's (Cookies, Green Monké) and

- Electric Brands (Sweet Justice).

(source)

But the real "moonshot" for us is the much larger US market, where we think PKP can replicate its market leading Canadian business model into a much larger market (when the industry grows, has regulatory certainty and is big enough).

We think the growth opportunity in the US will become a lot clearer in November 2026 - which is the deadline for federal hemp laws.

We think that, depending on what regulation is put in place it could be transformative for PKP’s US business.

See more on this risk in our last PKP note here: PKP: Business turnaround is kicking in? 1.4M units produced this quarter, up 56%.

A regulated US market is exactly the kind of market PKP, already the leader in the world's most regulated THC drinks market, is built to win in.

In recent years, the established companies actually want and welcome regulation, although it can create more barriers to operate, these same barriers can make it near impossible for competitors to enter the market.

For now, the Canadian side is doing the heavy lifting on what today's numbers show: more volume, lower costs, positive EBITDA, is the proof of execution we wanted to see.

What we want to see next from PKP

There are three major catalysts we're watching over the next 6–12 months:

Continued production ramp toward 12M unit Canada capacity

Each quarterly update will show whether the ~47% utilisation is improving further. Ideally, throughout the quarter we will see PKP sign more partnerships in Canada.

Here are the milestones we are tracking:

- 🔄 Q4 FY26 production: ~1,500,000 units (confirmed purchase orders in hand)

- 🔲 Continue filling Canada capacity toward ~75%+ utilisation

- 🔲 Additional new brand partnerships announced

- 🔲 Further OCS listing acceleration in next call

US operations update

This is the one we are most looking forward to.

Here are the milestones we are tracking:

- ✅ Florida facility opened

- ✅ Envision Emulsions lab commissioned at Florida facility

- ✅ First US sales: 680,000+ cans in H1 FY26

- ✅ Funky Buddha deal signed

- 🔲 More manufacturing deals signed.